Personal budget: manage your household finance

This blog post covers the essentials of personal budgeting in the UK, explaining what a personal budget is and how to understand your income and expenses, including common overlooked costs and discretionary spending. It guides readers on setting financial goals, planning for irregular expenses, and introduces several budgeting strategies such as the 50/30/20, 70/20/10, 60/10/10/10/10 rules, and the envelope method.

Managing your money effectively starts with a simple yet powerful tool, personal budgeting. When you clearly understand where your income goes, you can avoid financial stress, improve your savings, and make more intentional decisions with your money. Rather than feeling restricted, budgeting offers financial freedom: it gives you control over your finances instead of letting your money control you.

In the United Kingdom, households are increasingly looking to take control of their finances. Building a solid budgeting habit can help you navigate both everyday expenses and future plans with greater confidence. With rising living costs, inflation, and economic uncertainty, having a personal budget is more important than ever for financial stability and peace of mind.

What is a personal budget?

A personal budget is a plan that outlines your income and expenses over a certain period, typically a month. It allows you to allocate money to specific categories such as rent, groceries, transport, and savings. By organising your finances into clear sections, you can see where you might be overspending and where you have room to save.

What is personal budgeting?

Personal budgeting is the process of tracking your earnings and spending to ensure that you live within your means. It is a proactive financial strategy to help avoid unnecessary debt and work towards financial goals—short-term and long-term.

Whether you’re aiming to save for a deposit on a house, build an emergency fund, or just feel more in control day-to-day, personal budgeting gives you a financial roadmap. It also helps you develop a habit of conscious spending, which can lead to improved money management over time.

Understand your income and expenses

To build a personal budget, begin by recording your monthly income (such as wages, benefits, pensions, or freelance earnings) and all household expenses. Being realistic and honest about your finances is essential.

In the UK, some common monthly outgoings include:

- Rent or mortgage payments – These are usually the largest single expense.

- Utilities – Includes electricity, water, gas, internet, and mobile phone plans.

- Council tax – This varies depending on your local authority and property band.

- Groceries – Supermarket shopping and household essentials.

- Transport – Costs for petrol, insurance, public transport, car tax, and maintenance.

- Subscriptions and memberships – Such as streaming services, fitness clubs, or magazines.

- Childcare or education costs – Nursery fees, school meals, or tuition support.

Consider using bank statements to review the last few months of spending. This helps build an accurate picture of your financial habits.

What are some common “money leaks” that are easy to overlook?

Small, irregular purchases can add up. These may include:

- Takeaway coffees or snacks: £3 here and there adds up to £60+ a month.

- Forgotten subscriptions: Unused streaming services or app renewals.

- ATM withdrawal fees: Especially from non-bank machines.

- Late payment charges: Easily avoided by setting reminders or automating payments.

- Impulse online shopping: One-click buys can lead to regret and clutter.

Tracking every pound helps you spot these leaks and plug them. Review your bank or credit card statements regularly to identify patterns and unnecessary charges.

What are some non-essential or discretionary expenses?

Discretionary spending refers to non-essential items and services such as:

- Dining out or takeaways – Nice occasionally, but costly when frequent.

- Streaming subscriptions – Do you use all of them regularly?

- Hobbies or leisure activities – Events, classes, or purchases related to personal interests.

- Upgrades to devices or vehicles – Replacing when not necessary.

- Gym memberships – Especially if you’re not attending regularly.

Recognising these costs allows for more flexibility when making adjustments. During tight months, reducing discretionary spending can free up funds for savings or emergencies.

Set financial goals and prioritise spending

Establishing clear financial goals gives purpose to your budget. These could include saving for a home, paying off credit card debt, or planning a family holiday.

To set meaningful goals, try using the SMART method: Specific, Measurable, Achievable, Relevant, and Time-bound. For example, “Save £1,000 for an emergency fund in 6 months” is more actionable than simply “save more money.”

Once your goals are set, categorise your spending into needs, wants, and savings/debt repayment, and prioritise accordingly.

Benefits of being mindful of your personal budget

Being intentional about your spending can help you:

- Avoid unnecessary debt – By knowing your limits and living within them.

- Prepare for unexpected costs – Through emergency savings.

- Build savings over time – For both short- and long-term needs.

- Reduce financial pressure – Less stress, more confidence.

- Focus on what truly matters to you – Whether that’s travel, education, or peace of mind.

Even small improvements can make a significant impact when maintained consistently.

How can I plan for irregular expenses?

Some costs don’t occur monthly but still require preparation. These may include:

- Holidays or travel – Flights, accommodation, spending money.

- Car maintenance and MOTs – Often annual but can be costly.

- Birthdays and seasonal gifts – Especially around Christmas or family celebrations.

Setting aside a small amount each month for these expenses, sometimes called a sinking fund, can prevent sudden disruptions. For example, if you expect to spend £600 on Christmas, saving £50 per month from January will have you fully covered by December.

Budgeting strategies

Different budgeting strategies offer flexible frameworks to manage your money depending on your lifestyle, income level, and goals. Choosing the right one can help reduce stress, build savings, and support both short- and long-term financial wellbeing.

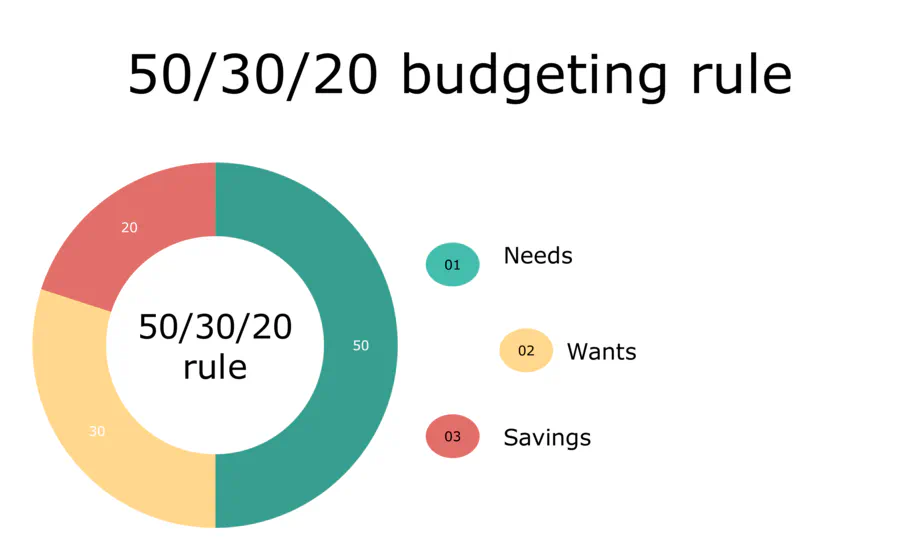

50/30/20 savings rule

The 50/30/20 rule splits your after-tax income into three categories:

- 50% for needs

- 30% for wants

- 20% for savings or debt repayment

This simple structure encourages balance and prioritisation. It’s especially popular among beginners due to its ease of application and broad flexibility.

The 50/30/20 budgeting rule: needs, wants and savings.

What are the origins of the 50/30/20 rule?

The rule was popularised by US Senator Elizabeth Warren in her book All Your Worth: The Ultimate Lifetime Money Plan, where it was promoted as a lifetime budgeting approach. It was developed as a response to overly complicated financial planning methods that often overwhelm individuals.

Where to allocate the money

- 50%: Needs – rent or mortgage, utility bills, insurance, groceries, transportation, minimum debt payments

- 30%: Wants – dining out, hobbies, streaming services, holiday travel, luxury upgrades

- 20%: Savings – emergency fund contributions, retirement accounts, investments, or paying down debts more aggressively

Practical example for the 50/30/20 rule

| Monthly After-Tax Income | 50% Needs | 30% Wants | 20% Savings |

|---|---|---|---|

| £1,000 | £500 | £300 | £200 |

| £1,700 | £850 | £510 | £340 |

| £2,400 | £1,200 | £720 | £480 |

| £3,200 | £1,600 | £960 | £640 |

Common mistakes

- Misclassifying wants as needs (e.g., designer clothes or luxury car payments)

- Ignoring irregular income or windfalls

- Failing to adjust categories as your life changes, such as after a job change, relocation, or family expansion

70/20/10 savings rule

The 70/20/10 rule recommends spending:

- 70% on needs

- 20% on wants

- 10% on savings

This model prioritises living costs while still encouraging consistent saving habits. It’s often favoured by those with tighter budgets or high living expenses.

Where to allocate the money

| Monthly After-Tax Income | 70% Needs | 20% Wants | 10% Savings |

|---|---|---|---|

| £1,000 | £700 | £200 | £100 |

| £1,700 | £1,190 | £340 | £170 |

| £2,400 | £1,680 | £480 | £240 |

| £3,200 | £2,240 | £640 | £320 |

Common mistakes

- Overspending on wants disguised as needs (e.g., premium versions of essential items)

- Infrequent review of financial priorities or ignoring rising costs over time

- Neglecting savings due to low allocation—requires strict discipline

60/10/10/10/10 savings rule

This model divides income into five distinct categories:

- 60% for needs

- 10% for an emergency fund

- 10% for retirement

- 10% for debt repayment or medium-term saving

- 10% for leisure or discretionary spending

This approach emphasises comprehensive financial security by separating long-term and short-term savings.

Where to allocate the money

| Monthly After-Tax Income | 60% Needs | 10% Emergency | 10% Retirement | 10% Debt/Medium-Term | 10% Leisure |

|---|---|---|---|---|---|

| £1,000 | £600 | £100 | £100 | £100 | £100 |

| £1,700 | £1,020 | £170 | £170 | £170 | £170 |

| £2,400 | £1,440 | £240 | £240 | £240 | £240 |

| £3,200 | £1,920 | £320 | £320 | £320 | £320 |

What if my needs exceed 60% of my income?

If your essential expenses surpass the 60% threshold:

- Consider downsizing housing or vehicle costs

- Look for ways to cut costs, such as switching to budget providers or meal planning

- Explore options to increase your income, through side hustles, upskilling, or asking for a raise

- Temporarily reduce other categories, such as leisure or medium-term savings

Common mistakes

- Treating emergency savings as discretionary and using them prematurely

- Underfunding retirement due to more immediate financial pressures

- Focusing too much on wants while ignoring growing debts

The envelope system rule

The envelope system is a physical, cash-based method of budgeting. It requires dividing money into envelopes labelled by spending category (e.g., groceries, petrol). It’s highly visual and tactile, ideal for those who prefer physical control over money.

How does the envelope method work?

- Categorise Your Expenses – define core categories like groceries, transport, dining out

- Label Envelopes – assign one envelope per category

- Allocate Cash – withdraw your monthly budget and divide it accordingly

- Spend as Needed – use only what’s in each envelope for its purpose

- Avoid Overspending – once an envelope is empty, spending in that category stops

Additional considerations

- Cash Only – requires consistent access to cash and physical envelopes

- Security Concerns – physical money is vulnerable to loss or theft

- Tracking and Management – no digital record; you must manually note transactions

- Modern Adaptations – digital envelope systems exist via apps and prepaid cards for convenience

Common mistakes when choosing a household budgeting rule

- Selecting a rule that doesn’t suit your lifestyle, income frequency, or financial obligations

- Being too rigid and not allowing for flexibility when unexpected expenses arise

- Not adjusting your budget as financial circumstances change, such as after a raise or family changes

- Failing to track spending habits, which leads to budget leaks

- Neglecting long-term goals in favour of short-term comfort

Review and adjust your budget regularly

A static budget quickly becomes outdated. As your life circumstances shift like changes in income, new expenses, or evolving goals, so should your budget. Regular reviews ensure that your financial plan stays practical, efficient, and aligned with your values.

How often should I review my spending habits?

Consider reviewing:

- Weekly for new budgeters

Get into the rhythm of tracking every penny. Weekly reviews help reinforce habits, spot trouble areas early, and build confidence. - Monthly for regular check-ins

Ideal for those with a consistent income and spending pattern. Reconcile bank statements, check progress on goals, and adjust where needed. - Quarterly for larger life or income changes

Use quarterly reviews to reflect on broader trends, like seasonal expenses, salary changes, or lifestyle shifts. This helps realign your strategy with longer-term goals.

4 tips to be consistent

- Set reminders to review your budget: Use calendar alerts to prompt reviews—treat them like important appointments.

- Use budgeting spreadsheets: A simple Excel sheet can simplify tracking and visualization.

- Celebrate small wins to stay motivated: Paid off a credit card? Met your savings target this month? Reward yourself in meaningful, budget-friendly ways.

- Adjust categories based on your life changes: Getting a dog, starting a new hobby, or facing rising grocery prices? Make room in your budget accordingly.

Savings and debt repayment

A well-structured budget supports better savings and smarter debt repayment. By allocating income purposefully, you gain control over both your short-term cash flow and long-term financial health.

Emergency fund

Aim to save 3–6 months’ worth of essential expenses to cover unexpected events like job loss, medical emergencies, or urgent home/car repairs. Start small if needed, consistency is key. Keep this money in a separate, current account to avoid dipping into it unnecessarily.

Debt repayment

Prioritise high-interest debts, such as credit cards, to reduce the amount you pay over time.

Two popular strategies:

- The Snowball Method: Pay off the smallest debts first to build momentum.

- The Avalanche Method: Tackle debts with the highest interest rates to save more in the long run.

Make sure minimum payments are covered for all debts while applying extra funds to your chosen target.

Saving for medium-term goals

These are goals you plan to reach in 2–5 years.

Examples:

- A house deposit

- A wedding or honeymoon

- Career development or education

Open a dedicated savings account for each goal and automate contributions where possible. Use tools like sinking funds to stay on track.

Preparing for retirement

Even if retirement feels far off, the earlier you start, the more your money can grow thanks to compound interest.

In addition to your workplace pension, explore:

- Individual Savings Accounts (ISAs)

- Self-Invested Personal Pensions (SIPPs)

- Robo-advisors

Regularly increase contributions as your income grows and review your investment strategy periodically.

FAQ

How do I start budgeting if I have variable income?

Base your budget on your lowest average income month and adjust as extra money comes in.

Is it better to save or pay off debt first?

If your debt has high interest, it’s generally wise to pay it down first. Otherwise, a balance of saving and repayment is helpful.

What tools can I use to budget?

Spreadsheets, or even pen-and-paper can be effective. Choose what you’ll stick with.

Final thoughts

Personal budgeting is a practical tool that can help every household in the United Kingdom make more intentional financial decisions. By understanding your income, controlling expenses, and choosing a budgeting strategy that fits your lifestyle, you can work toward both short- and long-term goals.